Financial Management

The financial management process encompasses the financial and operational management of UNDP’s implementation of Global Fund programmes, and is structured as follows:

- Grant-making and signing

- Grant implementation

- Sub-recipient management

- Grant reporting

- Grant closure

This section is primarily intended to serve as a guide for UNDP Country Offices (COs) that are acting as interim Principal Recipient (PR) to Global Fund grants and for those COs who have signed a Financing Agreement to provide technical support to recipients of Global Fund funding (e.g. Principal Recipient, Sub-recipient). This section also contains guidance for UNDP COs that are recipients of Country Coordinating Mechanism (CCM) funding.

Financial management processes are directly associated with other substantive areas of the Manual. Appropriate links to these sections, and to other UNDP and Global Fund documentation, are provided throughout. Global fund projects adhere to UNDP’s Financial Regulations and Rules and UNDP's Internal Control Framework in all instances. In addition, the Global Fund Operational Policy Manual is an important reference tool.

Grant-Making and Signing

The Grant Confirmation is the legal instrument which forms the basis of the contractual obligation between the Global Fund and the PR. During the grant-making process, the Country Coordinating Mechanism (CCM) and the Global Fund work with the PR to develop, among other documents:

- the performance framework

- the detailed budget

- the work plans

- the health products management template (HPMT)

The overall funding process is summarized in the Global Fund’s Applying for Funding section.

Please refer to the Legal Framework section of the Manual for a detailed analysis of relevant legal agreements.

Prepare and Negotiate Work Plan and Budget with the Global Fund

The Global Fund’s allocation-based funding model uses a modular approach and costing dimension that enhances the linkage between programmatic and financial information. Interventions and activities are defined in the modular approach and the cost groupings and cost inputs in the costing dimension (budgetary framework). This approach provides applicants and implementers with a standardized costing dimension that allows for resource allocation, the setting of realistic goals for each defined period of the grant life cycle, strengthened tracking of budget versus expenditure data and the alignment/harmonization of partners and country data systems. Each module is linked to a specific disease and each intervention is linked to a module. Refer to the Global Fund Guidelines for Grant Budgeting and the Modular Framework Handbook for further guidance.

Global Fund budgeting principles can be summarized as follows:

- The budget must be denominated in either Euros (€) or US dollars ($) as communicated by the country to the Global Fund. However, the budget should be prepared using the different currency denominations of each budget line, i.e., the currency in which the budget item will be paid. The currencies should then be converted into the grant currency at an appropriate exchange rate.

- Budgets should include not only costs for programme activities but also take into consideration any relevant income generated through activities and on programme assets.

- Budgets should be presented with the following attributes, which together determine the reasonableness of individual budget lines and the total grant budget. The budget should:

- ensure the economy, efficiency and effectiveness (value for money and prioritization of interventions that drive health outcomes);

- be built on budget categories defined by the Global Fund for the list and definition of Global Fund cost categories (see Global Fund Operational Guidance for Grant Budgeting);

- be consistent with the budget submitted with the funding request and reflect any Technical Review Panel (TRP) and Grants Approval Committee (GAC)-proposed adjustments;

- include any requirements mandated by the Board (for example, inclusion of Green Light Committee fees for approved multidrug-resistant TB programs);

- not duplicate costs covered by other sources of funding (other donors, government subsidies, etc.);

- clearly identify reasonable quantities and unit prices;

- be consistent with proposed programmatic targets defined for each time period;

- reflect a realistic rate of utilization of funds, taking into consideration absorption capacity of the PR and other grant implementers, including procurement and other deliverable lead-times;

- be arithmetically accurate; and

- fall within the available maximum allocation amount for the disease component as adjusted in the approved programme split and any above-allocation funding approved by the Global Fund.

Detailed guidelines area available in the Global Fund Guidelines for Grant Budgeting.

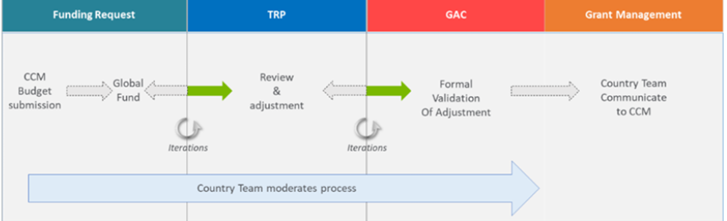

Prepare Funding Request

The initial step in the funding process is the development of a funding request for a disease component by all stakeholders, in the context of the CCM governance mechanisms. In preparation for the development of the funding request, the applicant chooses a proposed start date for the implementation period of the new funding request. The applicant will need to be aware of the upper limit for grant-making, taking into account the funding forecast available at the start date of this period.

Initial “best estimate” budgets by intervention are the minimum requirements for the submission of the funding request. The budget at the funding request stage is not detailed, but it serves to provide the strategic investment and intervention choices. It should be based on both realistic requirements to meet targets and the total amount of grant funds available.

The following are the key information requirements for budgets at this stage:

- A description of the intervention, including details of the target population and geographic scope, the implementation approach, and other relevant information pertaining to the intervention;

- The annual funding required for each intervention, including the following qualitative details:

- cost assumptions (e.g., latest historical cost, quotations provided by vendors etc.);

- reference to development partners costing tools (where applicable);

- outline of additional sources and amounts of funding available for each intervention, with a distinction of the requests by “Within the allocation” (based on total approved programme split of the country for a specific disease) and “Above-allocation” (which covers the full expression of needs for effective disease programme implementation in the country, covering all existing funding gaps); and

- Proposed implementing Principal Recipient(s)(PRs) and Sub-recipient(s) (SRs) (if available).

It may be more convenient to prepare a more detailed budget at the funding request stage, which can then be consolidated into an intervention-based budget for submission to the Global Fund (for example, in cases where the latest historical costs of certain known activities in an intervention are already available).

Please see here for detailed information on the budget approval process.

The diagram below provides a summary of the stages of the budgeting process for the funding request.

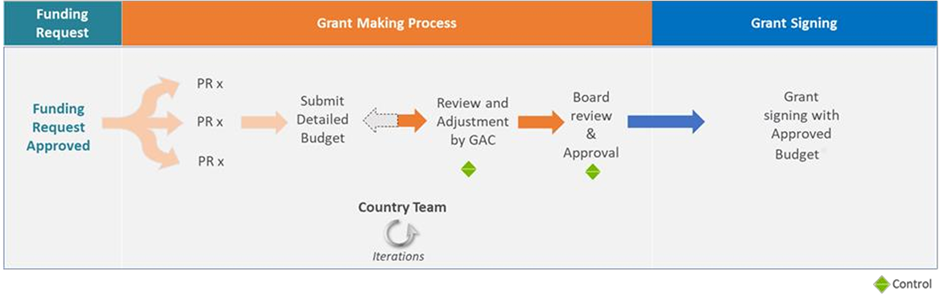

Prepare and Finalize a Global Fund Budget during Grant-Making

Once a funding request is recommended for grant making, the nominated Principal Recipient (PR) is required to develop a detailed budget using the full modular approach and costing dimension. Each PR must submit a detailed budget for review and approval, as indicated in the diagram below.

Practice Pointer

Practice PointerNOTE: under Grant Cycle 7 (GC7) – 2023-2025 GF Allocation Period – the Detailed Budget template comprises two worksheets – one for health products (Detailed Budget – Health Products for Cost Groupings 4, 5, 6, and 7) and another for non-health products (Detailed Budget – Non-Health Products for all Cost Groupings except 4, 5, 6, and 7). Depending on the type of portfolio (High Impact, Core, Focused), the Global Fund Country Team will confirm whether a HPMT is required and, in such cases, the HPMT must be finalized first, and then the data copied/pasted into the Detailed Budget – HP worksheet of the DB template. The HPMT includes a Detailed Budget worksheet that includes all required information and is structured to mimic the Detailed Budget – HP worksheet. The PR will not be able to edit the information in the Detailed Budget – HP worksheet. When an HPMT is not required, the Detailed Budget – Non-HP worksheet is used exclusively for all budget lines across all cost groupings.

In addition, the PR is encouraged to design the work plan and annual budget (with detailed cash forecasting for each quarter). It is also recommended that the Country Office (or a grant designing team) should take the following into account in the template:

Transition between Allocation Utilization Periods

The grant allocation can be used for activities that were budgeted, approved and completed during the grant implementation period associated with the country’s allocation – regardless of whether the payment for such activities has occurred. The following principles apply:

- Financial commitments are current contractual obligations to pay a specified amount of cash against goods and services already received, but for which the related payment has not yet been made (all or partial). Financial commitments existing at the end of a grant implementation period can be paid from that period’s allocation (via available cash balance or a disbursement from the Global Fund) and must be liquidated no later than six months after the end of the grant Implementation Period (unless otherwise approved in writing by the Global Fund).

- Financial obligations are current contractual obligations to pay an agreed amount of cash (i.e., as per signed contract and/or purchase order) to a third party for the provision of goods/services at a certain point of time in the future, i.e., the goods or services are yet to be received. Financial obligations existing at the end of an implementation period cannot be paid from that period’s allocation and must be transferred and included in the budget of a new grant or an extension, to be covered by funds from the next allocation.

Therefore, all financial commitments existing at the end of the current Allocation Utilization Period will be paid from the current allocation, while financial obligations existing at the end of the current Allocation Utilization Period will be funded from the next implementation period allocation. These amounts will need to be considered in the negotiation of the next grant and included in the budgeting and programmatic planning for the next allocation utilization period.

In certain cases, payments relating to goods and/or services delivered after the end of an Allocation Utilization Period may be considered financial commitments to be funded from that Allocation Utilization Period, where the following three criteria are met:

- the implementing entity has placed the order(s) for the goods or services at issue with adequate consideration for relevant lead times1 such that the goods or services were expected to be delivered before the end of the allocation utilization period; and

- the delivery of the goods or services is delayed for reasons beyond the implementing entity’s control; and

- the delivery of the goods or services is completed within a maximum of 90 days of the Allocation Utilization Period end date.

Six months after the start of the new Implementation Period2, Principal Recipients will be required to report3 the final available cash balance from the previous allocation period (after all financial commitments are fully paid). Any unliquidated commitment remaining at the end of the six-month period will be considered closed by the Global Fund unless otherwise approved in writing by the Global Fund.

Upon the signing or modification of grant confirmation, final in-country cash balance amounts may be deducted from the grant funds amount of the new grant as stipulated in the grant confirmation. Consequently, in-country cash balances from the previous Implementation Period may be deducted from the future funding (disbursement) decisions of the Global Fund.

For grants in closure or already closed prior to the allocation period, the Principal Recipient is required to reimburse the cash balance directly to the Global Fund, unless otherwise approved in writing by the Global Fund.

Detailed guidance on transition from the old to the new allocation funding and relevant budgeting and reporting requirements is available in Global Fund Guidelines for Grant Budgeting, Global Fund Operational Guidance for Grant Budgeting and in the Global Fund Operational Policy Manual (Section 3: Implementation Period Reconciliation and Grant Closure).

Foreign exchange

Budgets of Global Fund grants are either finalized in Euros (€) or US dollars (US$), depending on the new funding model allocation currency choice, considering the payment currency for each budget line. The allocation currency should be requested by the applicant no later than 30 days after the issuance of the allocation letter to the country. Global Fund grant budgets should be prepared using the different currency denominations of each budget line (i.e., the currencies in which the budget item will be invoiced or charged) converted, where applicable, to the currency of the Grant Confirmation at an appropriate exchange rate.

Any inflation factor should take account of the currency denomination of the budget item (local currency-denominated items may require a different rate of inflation to foreign currency-denominated items). The relationship between the two variables—exchange rate and inflation rate—should be described in the general budget assumptions.

The exchange rate used in the budget should be that which, based on available evidence, reflects the best estimate of the rate at which the PR will exchange their grant currency into local currency over the term of the grant. The method and/or references used should be fully disclosed in the general budget assumptions. The exchange rate may be budgeted at different rates over the term of the budget, provided that assumptions behind the rates are disclosed. No exchange rate “contingencies” may be included in the budget. If the country’s exchange rate is fixed or managed by the domestic authorities, the budget should follow the given official fixed rates.

Taxes

Global Fund funding is made available based on the principle that grant funds are exempt from relevant taxation imposed by the host country concerned. The required tax exemption for Global Fund purposes mainly includes (but is not limited to): (a) customs duties, import duties, taxes or fiscal charges of equal effect levied or otherwise imposed on the “Health Products” imported into the host country under the Grant Confirmation or any related contract (collectively “Custom/Import Duties”) and (b) VAT levied or otherwise imposed on the goods and services purchased using grant funds.

The obligation of the host country to provide tax exemption is mandatory and applies to the Global Fund programmes implemented partially or wholly by any Principal Recipient (PR) or Sub-recipient (SR) that is not a “Government Entity.” In administering the tax exemption, if needed, the PR should ensure an adequate follow-up of taxes paid and recovered at SR level.

The budget submitted to the Global Fund should be net of taxes on applicable unit costs. When tax exemption is obtained on a reimbursement basis (i.e., the PR must pay the taxes first and then claim reimbursement), the first year’s budget may include a provision related to the cash flow needs if required. This should be requested in the budget and supported by precise cash flow forecasts related to tax payment and recoveries. If the UNDP CO operates on a VAT reimbursement basis based on local legislation, UNDP CO shall try to ensure through coordination with the government of the Host Country and the CCM or, as the case may be, the relevant Regional Coordination Mechanism (RCM) or Regional Office (RO) and otherwise that the relevant Grant Agreement and the assistance financed thereunder shall be free from taxes and duties imposed under laws in effect in the Host Country.

Costs

Salary top-ups and travel-related costs

Allowances for salary incentives, top-ups, travel per diems and transportation costs are not paid from grant funds unless provided for in the funding request and grant agreement. If such schemes are indispensable for service delivery, applicants should include a valid funding rationale for such incentives as part of the funding request. The assumptions tabs in the Global Fund budget template are used for this justification.

Shared costs

Shared costs are expenses that can be allocated to two or more funding sources (government, the Global Fund, other donors etc.) or different Global Fund grants based on shared benefits and administrative efficiency. These costs are allowed when they are:

- verifiable from implementers’ records with evidence on “fair share” principle;

- necessary and reasonable for proper and efficient accomplishment of grant and programme objectives;

- included in the approved budget when required; and

- expensed during the grant implementation period.

The apportionment method must be clearly stipulated in the budget assumptions.

Budgeting for Project Management Unit (PMU) and other staff costs

The Global Fund budget template contains three types of assumption tabs:

- Travel-Related Cost grouping of cost-inputs;

- Human Resources grouping of cost inputs; and

- All others.

The related assumption tab is used for each detailed unit cost.

Staff costs are calculated and budgeted as follows:

- UNDP’s Pro-forma Costs for Fixed Term Appointment (FTA), Technical Assistance positions either on Temporary Appointments or Personnel Service Agreements.

Note that all information related to the procurement of health products – i.e., the list of health products, unit costs, quantities, and associated procurement and supply management (PSM)-related costs – are captured in the Health Product Management section of the Manual.

Practice PointerCost recovery

In preparing the budget, the Principal Recipient (PR) should include all relevant direct costs and indirect overhead costs.

The PR is responsible for negotiating any indirect and overhead costs to be charged by Sub-recipients (SRs) and other implementing entities. If such entities are international nongovernmental organizations (NGOs), the relevant indirect cost recovery policies on SR costs apply. Local NGOs should include all charges as direct costs.

When formulating Global Fund budgets, UNDP policy is adhered to with respect to cost recovery. UNDP distinguishes between two types of costs in the implementation of its activities. These are:

- Costs that are in addition to direct project costs, representing the costs to the organization that are not directly attributable to specific projects or services, but are necessary to fund the corporate structures, management and oversight costs of the organization. These costs are recovered by charging a cost recovery rate, known as General Management Support (GMS) fee; and

- Direct Project Costs (formerly known as DPC, currently renamed Delivery Enabling Services, DES) - direct costs of programme, administrative and operational support activities, that are part of the project input.

General Management Support

GMS is defined as indirect costs incurred by an organization as a function and in support of its activities, projects and programmes. The key feature of these costs is that they cannot be traced unequivocally to specific activities, project or programmes.

Based on the exceptional approval of UNDP’s Executive Board for existing corporate framework agreements, the GMS rate between the Global Fund and UNDP is 7 percent. The agreed percentage fee for GMS between UNDP and the Global Fund is corporately agreed, and as it is Executive Board legislated, it is non-negotiable. GMS is to be categorized as overhead and included as a budget line for all grants. This GMS rate is applicable for the Principal Recipient role and when UNDP is providing technical support to a Global Fund Principal Recipient or Sub-recipient through a Financing Agreement. Any deviations to the GMS rate must be approved by the BMS Director prior to any negotiations with the donor. Refer to UNDP Programme and Operations Policies and Procedures (POPP) on Resource Planning and Cost Recovery for detailed guidance on GMS, and in case of specific queries, reach out to the GFPHST Finance Team or Programme Team.

Direct Project Costs (or delivery enabling services)

Detailed budgeting guidance

Detailed budgeting instructions can be obtained from the Global Fund Operational Guidance for Grant Budgeting under the following areas:

- Human resources, including salaries, allowances and accrued severance entitlements;

- Travel-related costs;

- External professional services;

- Pharmaceutical, non-pharmaceutical health products and health equipment;

- Infrastructure and non-health equipment;

- Communication material and publications;

- Management fees and indirect cost recovery; and

- Living support to client/target population (Microloans and micro grants; cash incentives).

Budget approval

The funding request budget and the detailed budget prepared for the grant-making process should be uploaded to the Global Fund’s online platform [the latest platform is Grant Operating System (GOS)].

A standardized detailed budget (DB) template is extracted from the Global Fund’s GOS in Excel, with prepopulated data. The level of detail included in the DB Template shall differ depending on the stage of the application, i.e., whether the application is at funding request or grant-making stage.

The summary budget is automatically produced in the DB template for all stages of the budgeting mechanism (e.g., funding request, grant-making, reprogramming). The summary budget reflects the costs of each intervention (modular approach) and cost grouping using standard budget classifications provided in the costing dimension (cost inputs/cost grouping).

To ensure efficient and timely review and approval, when submitting a budget for approval the Principal Recipient (PR) should include all unit cost assumptions and upload all relevant supporting documents. The estimated time for the review and approval of the detailed budget submitted by the PR is 30 to 90 days, depending on the stage of the process. Additional clarifications and/or budgets that do not comply with Global Fund principles could lead to additional delays in the approval process.

Once approved, the budget is captured in Global Fund systems as the official approved budget and used as the basis for financial reporting unless it is modified through the grant agreement after any material budget adjustments. This is also the “baseline budget” and all budget adjustments will be compared against this version for the establishment of materiality thresholds.

Secure Banking Arrangements

UNDP uses only two bank accounts (U.S. dollars (US$) and Euro) for receiving contributions from the Global Fund.

Prior to Board approval and/or signing of the Grant Confirmation, the Global Fund undertakes the process of bank verification and authentication by requesting the details of the bank account of the Principal Recipient (PR) into which the grant disbursements will be deposited. Country Offices (COs) should request bank account confirmation letters from the UNDP’s Global Fund Partnership and Health System (GFPHST) Finance team.

Contributions will be credited to the bank account identified on the Face Sheet. The Global Fund disburses funds directly to the PR and they should clearly reference the applicable Grant Number in all deposits.

Country Coordinating Mechanism (CCM) and Financing Agreement funding should also be deposited in the HQ Contributions Bank Account.

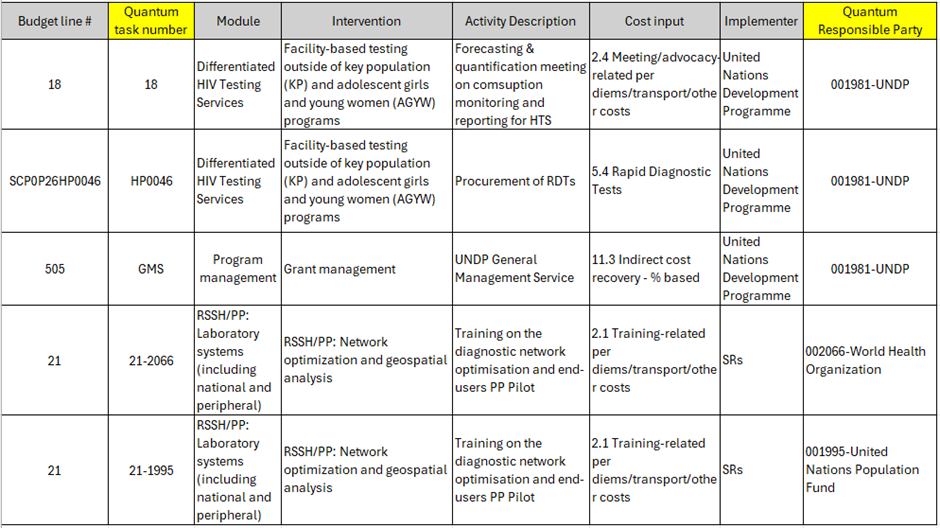

Project and Budget Formulation in Quantum

UNDP’s standard procedures as advised in UNDP Programme and Operations Policies and Procedures (POPP) - Project Design should be followed for Global Fund project and budget formulation. This includes guidance on how to ‘Formulate Programmes and Projects,’ ‘Select Responsible Parties and Grantees' and ‘Appraise and Approve.’ For more information on selecting Sub-recipients, please refer to the Sub-recipient Management section of this Manual.

It is important to remember that the term “Project” in UNDP policy represents the project document. Therefore, there may be one Project with multiple Outputs (“Projects” in Quantum). The budget control on budgets in Quantum (revenue, expenses, advances, etc.) is at the output level and NOT at the Project level.

Global Fund project/budget setup in Quantum should adhere to the following principles:

- Projects created in Quantum should conform to the standard structure that one Global Fund Grant Agreement corresponds to one Quantum Project with one Quantum Output.

- Country Offices (COs) should not create multiple outputs for one grant as this complicates cash management and cash reconciliation reports in Quantum. Only if the grant has an allocation from the Global Fund for COVID-19 (C19RM) activities, a second output can be added within the existing project.

Practice PointerIn some cases, the Global Fund may request UNDP to act as the Fund Administrator for Global Fund resources that are managed by the National PR. For such cases the Fund Code is 30078 and the Donor Code is 000327 should be used.

Country Coordinating Mechanism (CCM) funding (Fund 30068 Donor 000327) should have a separate project and output from main grant funding (Fund 30078 Donor 000327).

All Financing Agreements, signed between UNDP and the national PR with funding from the Global Fund should be budgeted and funded using fund code 30085 and the respective Donor code of the respective Government.

The proposal and project are created in Quantum Project Management Module (for guidance refer to UNall Knowledge Bases>Quantum>Project & Portfolio Management

* UNDP as Principal Recipient (PR) assumes the role of Implementing Partner (Direct Implementation - DIM) and is reflected in Quantum, when creating the Project, Financial Plan and Award under the “Institution ID” field (Institution ID - 99999).

* Where UNDP serves as Responsible Party, it should be reflected in the Implementing Agent field in Atlas (Implementing Agent - 001981).

When UNDP is the PR, COs use a set of budget account codes in Quantum, which correspond to the nature of expenses of the respective activity of the Global Fund Detailed Budget.

When UNDP is the PR, COs use a set of budget account codes in Quantum, which correspond to the nature of expenses of the respective activity of the Global Fund Detailed Budget.

Prepare and Negotiate Advance Payment Mechanism

The advance payment mechanism allows the Global Fund to approve a list of expenditures the Principal Recipient (PR) may incur before grant signing. Expenditures agreed to between the Global Fund and the PR during grant negotiations will be reimbursed when the Grant Agreement has been signed and the first disbursement has been released. The PR includes the approved grant making expenditures in the final grant budget.

To utilize the pre-allocation budget, a UNDP initiation plan shall be prepared and approved by the Local Project Appraisal Committee (LPAC), and a project established in Quantum (the same project to be used for grant implementation). Refer to section on Principal Recipient start-up for detailed guidance on pre-allocation budgets and UNDP initiation plan.

Pre-allocation activities must be funded from a Country Office (CO)’s own resources (such as Target for Resource assignment from the core (TRAC)) until subsequent reimbursement from the Global Fund. The project budget will thus initially include both sources on funding: UNDP fund code and Global Fund fund code. Upon receipt of Global Fund reimbursement, previously incurred expenses will be reversed in Quantum from the originally recorded fund code to the Global Fund fund code.

Procedures should be as follows:

- If possible, the reversals should be done per each transaction. If, however, too many transactions are involved, the option of a lump sum through one reversal could be considered, with the detail of all transactions maintained for reference.

- Any outstanding advances issued to Sub-recipients (SRs) should also be reversed by amending the initial invoice, unless otherwise instructed by OFRM or GSSC.

- Once the expenditures and outstanding advances have been reversed, the CO/PR should then proceed to reverse/zero out the budget under the UNDP fund code.

Grant Implementation

Revenue Management

UNDP’s revenue management policies and procedures with respect to non-core resources are summarized below. These policies ensure that revenue is recorded, receivables are raised, and the handling of cash and receipts and the application of income is consistent, timely and accurate.

- Revenue is recognized upon signature of the contribution agreement by both parties. Instalments are recognized as revenue based either on dates in the schedule of payments of the agreement, or the clause in the agreement that governs when an agreement becomes binding. For Global Fund grants, revenue is recognized upon signature of the Grant Agreement if there are no major deviation from the GF framework agreement and grant confirmation letter.

- Therefore, it is important that the Country offices to submit the grant agreements, its amendments to The Global Shared Service Centre (GSSC) through UNall.

- Country Offices (COs) submit all agreements and any necessary supporting documents as soon as possible through UNall

- The GSSC reviews the donor agreement submitted thru UNall and enters it in Quantum. The GSSC records revenue and creates the accounts receivables based on the projected cash disbursement milestones and conditions in each agreement. The contract is recorded in the currency indicated in the agreement. After the contract is created by the GSSC, the Contracts Module generates a contract reference number and communicated to the CO by the GSSC.

- Application of grant funds against Accounts Receivable (ARs) is handled by GSSC.

- Where an agreement has been amended with the approval of the donor, such amendment needs to be communicated to GSSC staff via UNall in a timely fashion. The GSSC then reflects these amendment(s) in the Contracts Module. A copy of the amended agreement should be uploaded to the DMS for the GSSC to process the amendment.

- COs should regularly review the Quantum revenue management reports, pending milestones and proactively follow up with the GF in order to receive the funds on time.

- It is important that COs promptly submit a request in UNall if there are any changes to the agreements or completion of milestone conditions, to ensure that revenue is accurately and completely recorded in financial statements.

Refer to the following guidelines:

- UNDP POPP on Non-Core Contributions

- UNDP POPP on Revenue Management Guidance: Global Fund Revenue

- UNDP POPP on Revenue Management Accounts Receivable

The process with respect to the Global Fund is detailed in the next sections. The same process would also apply to CCMs, FAs and Fund Administrators.

Global Fund Funding Decisions and Disbursements

The annual funding decision (AFD) and disbursement processes are critical grant management functions of the Global Fund. These processes allow the Global Fund to commit and disburse approved grant funds appropriately and take action to ensure grants continue to achieve maximum impact. There are two main objectives:

A. Decide on Annual Funding: Determine and commit the amount of funding that will be disbursed to the grant over the next 12 months of implementation1 (plus a buffer period, up to 6 months), considering implementation performance, issues, and risks; and

B. Disburse Funds: Disburse funds committed through the AFD to the Principal Recipient (PR), or third party on behalf of the PR, for the payment of goods and/or services.

The AFD and disbursement processes ensure:

- grant funds are used for agreed objectives and outputs in an accountable manner whereby known or new risks are minimized and mitigated;

- AFDs consider grant and PR performance to ensure PRs focus on results and timely grant implementation;

- AFDs are well documented and justified; and

- Disbursements are released on time to implementers and third parties to ensure the continuation of grant activities.

The processes of submitting the cash disbursement requests and the GF’s internal process of determining the AFDs can be found in the Global Fund Operational Policy Manual: Make Annual Funding and Disbursement Decisions.

Process Metrics for Annual Funding Decisions and Disbursements

UNDP and the Global Fund are expected to meet the following key performance indicators:

- 85% budget utilization (as per the Global Fund criteria) of the first year of implementation, reported at end-June/end-December [1];

- 94% budget utilization, reported in end-June/end-December [2];

- 90% disbursement utilization, reported in end-March/end-September;

- AFD Notification Letter sent by CT within 15 days [3] of AFD approval; and

- Disbursement Notification Letter sent by CT within 15 days of release of the disbursement.

[1] Budget utilization is reported annually for Focused portfolios.

[2] The amount committed under the AFD does not include centralized commitments and disbursements.

[3] All references to “days” in this document shall mean calendar days, unless otherwise stated.

Disbursements

A disbursement is the actual transfer of cash from the Global Fund to the Principal Recipient (PR) (in the currency(ies) of the signed Grant Confirmation) for the payment of goods and services. The disbursement schedule and forecasted amounts will be established by the Global Fund Country Teams as an integral part of the annual funding decision process.

The Global Fund Country Teams are responsible for ongoing grant monitoring and determining if circumstances have changed between the time of the AFD and the scheduled disbursements. Any changes to the originally approved dates and/or amounts for payees are completed through an approval workflow. Any such changes must be within the overall AFD.

A Disbursement Notification Letter is sent from the Global Fund Country Team to the PR to inform them of the disbursement. The Global Fund should clearly reference the applicable Grant Number in all disbursements. The Global Fund Country Team should provide additional contextual information to the PR if the relevant disbursement amount differs from what was originally approved in the annual funding decision. Upon receipt, UNDP Country Offices should submit promptly a request for a deposit application in UNall with the Notification of Grant Disbursement and Management Letter, if applicable.

For Country Coordinating Mechanism (CCM) funds (fund 30068 and donor code 00327), the Agreement is processed as a Global Fund Financing Agreement that will be submitted via UNall, indicating the start and end date. The CO is also required to provide a Schedule of Payment with dates or the best estimate dates of disbursement by the Global Fund if Schedule of Payment is not available.

For CCM agreements, the Global Fund makes cash transfers to cover the annual budgets of CCM secretariat considering the unspent cash balances from the previous reporting period. This is communicated to country offices and CCM via email by the Global Fund, hence, COs should ensure prompt submission of a deposit application request in UNall.

For Financing Agreements, it is recommended to have the payment schedules in the agreement. Upon notification from the donor on transfer of resources, the CO should submit a UNall case for a deposit application.

For further guidance please refer to the Global Fund Operational Policy Manual on Annual Funding Decisions and Disbursements

Revenue Management Processes

- The Principal Recipient (PR) negotiates an agreement with Global Fund, the donor, and incorporates a performance framework and summary budget. Once both parties agree, the Global Fund Grant Confirmation is signed.

- A designated Revenue Focal Point of UNDP Country Office (CO) will upload the signed face sheet of the active Global Fund Grant Confirmation, budget summary, performance framework and the first page (only) of the email from the Global Fund which has the Notification Letter attached to it thru UNall within 7 days of the last signature date. The Global Shared Service Centre (GSSC) will process this after ensuring that the correct Chart of Accounts information has been included in the Confirmation, as well as the total amount outstanding at the date of uploading the document.

- The GSSC will input the information from the Agreements into the Contracts Module where the accounting entries will be generated once the Letter of Notification has been received. Business units will be able to access reports with detailed information of all contracts created in the contract module and accounting entries processed.

- UNDP will submit a Progress Update/Disbursement Request (PU/DR) to the Global Fund to initiate the disbursement of funds.

- Once the PU/DR has been received and approved, a DR Notification Letter is received by UNDP from the Global Fund. This is immediately uploaded into the DMS by the Revenue Focal Point for the GSSC to trigger the accounting entries in the Contract Module as follows:

- DR Unbilled Accounts Receivables

- CR Revenue

- When the billing process starts based on the milestones achieved and the cash flow forecast, the following accounting entries will be triggered:

- CR Unbilled Accounts Payable

- DR Accounts Receivables

- Once the Notification of Grant Disbursement letter has been processed by the GSSC, they will send an email advising the CO of the Atlas Contract Reference number and the Accounts Receivable (AR) Item ID created. This information will be used by the GSSC when applying Global Fund disbursements.

- When the funds are received, cash is applied by Contribution Unit/Treasury and the accounting entries are as follows:

- DR Cash/Bank

- CR Cash Control

- On application of the Funds to Accounts Receivable:

- DR Cash Control Account

- CR Accounts Receivable Once the GSSC has processed the disbursement, they will create a Contract Reference number that will be entered into the Deposit/Disbursement Information section of the DMS. This reference number can be used by the Country Offices to look up the AR item ID in the Contracts Module.

- A query UN_IPSAS_RM_CA_PST_AR_ITEM_SUM is available in Atlas, which identifies the A/R Item ID based on the Contract number created for the Notification of Disbursements processed by the GSSC. Other Atlas revenue reports:

- The report Unapplied Contributions (UN Reports > Financial Management Reports > Revenue Management Reports > Unapplied Contributions shows contributions that have been received but not yet applied.

- The query UN_IPSAS_RM_APPLIED_DEPOSITS provides details of the deposits and AR items, and the projects to which they were applied. (Select a Tree “RM_CA_OP” and click on icon “Add to Node Selection List.”)

- Any amendments to agreements must be communicated to the GSSC as soon as possible. The amended agreement (e.g. Implementation Letters) must be uploaded to the DMS for the GSSC to update the Contracts Module and process any corresponding accounting entries.

- The following procedures should be adhered to at each period end:

- Check that all Confirmations have been uploaded into the DMS.

- Check that any amendments to Confirmation have been updated in the Contracts module by the GSSC.

- Follow up with donors on outstanding amounts where applicable.

- Ensure timely application of all unapplied deposits at year-end.

- Review funds received in advance account and verify accuracy and completeness.

Practice PointerInterest Revenue

Article 3(b) of the UNDP-Global Fund Grant Regulations states, “Any interest or other earnings on funds disbursed by the Global Fund to the Principal Recipient under this [Grant Confirmation] Agreement shall be used for Program purposes, unless the Global Fund agrees otherwise in writing.” In this respect, Country Offices (COs) should seek approval from the Global Fund for the use of interest or any other earnings and to ensure that such income is used for agreed programme activities.

Interest generated on Global Fund resources (except CCM and FA projects) is calculated by the Office of Financial Resources Management (OFRM) at year-end. The interest revenue is posted to the respective Global Fund projects in the current year at year-end in account ‘53045’ (Allocated Interest Income) and Donor ‘00327’ (Global Fund). (Note: Any adjustment or transfer of interest in subsequent years is recorded through GL account 51035.)

Interest recordings can be identified using the Account Activity Analysis (AAA) and Cash Balance Report. Interest earned for Global Fund projects must be reflected in the next Disbursement Request and Progress Update Report.

Interest earned in SR bank accounts is reported in the Funding Authorization and Certification of Expenditures (FACE) and recorded as per UNDP POPP procedures on Direct Cash Transfers and Reimbursements, step 1 :

“Any interest earned in bank accounts from advances provided by UNDP must be distinctly itemized on the FACE forms. For traceability and reconciliation purposes, the earned interest needs to be reported on the Combined Delivery Report (CDR), which is the official document used by auditors and government counterparts. However, the use of revenue account (5xxxx) will prevent the earned interest to be reflected in CDR reports. As a result, offices should record this earned interest through Zero Dollar Invoice (ZDI):

- When the interest is reported as earned by the partner (but has not been remitted to UNDP): Debit account 16005 (NEX Advances) and Credit account 74510 (Bank Charges) with the total amount of interest reported by the partner for a specific reporting period.

- When the interest is refunded to UNDP or utilized by the partner to cover project expenses: Debit the related Cash account 4xxxx) for refund; OR Debit Expenses (7xxxx) when the funds have been utilized; and Credit the NEX Advance account (16005)

The UNDP programme and finance team should ensure that the bank statement(s) are verified for evidence of the earned interest during assurance activities (audit or spot check).”

Practice PointerOther Revenue

Global Fund guidelines indicate that budgets should include not only costs for programme activities, but also take into consideration any relevant income generated through activities and on programme assets. Thus, all revenue-generating activities such as social marketing or sale of assets are to be addressed in the budget and reflected as revenue in all Global Fund reporting.

Social marketing - proceeds are recorded as Miscellaneous income by the Country Office (CO) under GL Account 55090, Fund Code 30078 and Donor 00327 (the Global Fund).

Disposal of assets - proceeds are recorded in GL account 55070.

Country offices should submit the deposit application requests in UNall.

Expenses Management

Under UNDP’s expense policy, expenses are recognized and recorded when goods and services are received by UNDP. A corresponding liability to pay is created at the time of recognition. The following categories of transactions are classified as expense:

- Goods (e.g., supplies)

- Services (e.g. utilities, consultants)

- Payments for Operating Leases

- Employee benefits (e.g., salaries, ASHI, leave)

- Use of plant, property and equipment (e.g. buildings, vehicles, computers depreciation)

- Finance costs (e.g., bank charges, fees)

- Transfers/grants (e.g., microfinance grants)

Refer to UNDP Programme and Operations Policies and Procedures (POPP) on Expense Management for detailed policies and procedures, including the following subject areas:

- Raising E-requisitions

- Creating and Approving Vendors

- Purchase Orders/Commitments

- Receipt of Goods/Services

- Accounts Payable

- Disbursing Funds (Making Payments)

- Regular Maintenance and Closure of Purchase Orders (POs)

- Regular Maintenance of Accounts Payable

- Petty Cash (PC)

- Prepayments

- Hospitality Expense

Prepayments

A prepayment is used when a supplier requires partial or full payment for goods or services prior to the delivery/provision of the goods or services. Examples would include one-off transactions for individual contracts, refundable deposits, construction works and long-term agreements (LTAs) for health products.

When paid, prepayments reflect as amounts due to UNDP and are recorded in the asset account 16065 (Prepaid Voucher Modality). As the goods or services are provided, the prepaid asset balance must be reduced and an expense recorded for the amount of goods or services received by UNDP. This is achieved by receipting and vouchering against the relevant Purchase Order (PO) and offsetting the prepayment against the Accounts Payable (AP) PO voucher. Such offsets need to be communicated to the vendor. Accounting procedures in Atlas/Quantum are as follows:

- Account 16065 Prepaid Expense is debited and AP credited for the amount of the prepayment.

- When a PO-AP voucher is created, the prepaid voucher is automatically offset against the PO-AP voucher, reducing the amount to be disbursed to the vendor.

- A PO must be created for the full amount of the purchase or contract (as if no prepayment is being made).

- Once PO exists, a Prepaid Voucher needs to be created for the amount of the prepayment. The PO ID must be entered as a reference in the Prepaid Voucher.

- Balance sheet account 16065 should be monitored on a monthly basis to ensure timely clearing of prepayments.

- Spot checks of payments to vendors with prepayments should be performed regularly to verify that no overpayments were made.

For transactions such as rent, maintenance and service contracts, and insurance premiums, where contracts are annual and amounts are relatively stable from month to month and from year to year, it is not necessary to raise a prepayment, even though payment will be made prior to receiving the services. These items can be processed via a regular PO with immediate receipting for the value of the prepayment required. At year end, the Office of Financial Resources Management (OFRM) will provide necessary guidance for any adjustments needed to reallocate expenses to prepaid assets, depending on materiality.

In addition, the following payments should not be treated as prepayments: security deposits; staff advances; non-refundable deposits; and advances to Sub-recipients.

Further guidance regarding prepayments can be found in the UNDP Programme and Operations Policies and Procedures (POPP) on Prepayments

An additional guidance note focusing on the procedures for processing prepayments to the United Nations Children’s Fund (UNICEF) under the LTA for the procurement of health products for Global Fund projects managed by UNDP where prepayment is required in full, are available also with the GFPHST. For more information please check the Health Product Management section of the Manual.

UNDP Inventory management

UNDP inventory policy requires qualified inventories to be recognized as assets until consumed or distributed. The balance of such inventories must be physically counted, valued, recognized and reported as assets at the end of each reporting quarter. The determination of items to be included in inventory is based on ownership and control of the inventories. The physical location or custody of the inventories are factors to be considered in determining control (i.e., whether they are stored on UNDP premises or managed by UNDP personnel). UNDP must recognize the inventories if UNDP undertakes any of the following responsibilities:

- Controls access to and distribution of the inventory items;

- Administers a programme requiring distribution of the inventory items (as opposed to situations where the inventory items are purchased solely for immediate shipment to a local government/implementing partner; or

- Bears the risks of loss, theft, damage, spoilage, etc.

Undistributed inventory over which UNDP has direct control and access, administers distribution or bears the risk of loss, theft, damage, etc. is reportable in UNDP’s financial statements. To satisfy the reporting requirement, Country Offices (COs) are required to count inventory and supplies at the end of each quarter and submit a certification of this to the UNDP Office of Financial Resources Management (OFRM) by the prescribed deadline. Detailed guidance for the physical count of inventory end is communicated by OFRM for the second quarter and year-end financial closure. OFRM then posts accounting adjustments for crediting expenses and debiting inventory account 14602 at the end of the reporting period (to capture the closing balances). These adjustments (as opening balances) are reversed at the start of the next quarter at a general ledger level without impacting the project expenses and resources in Quantum since 2023.

Inventory in transit is enroute goods purchased that are in the ownership of UNDP but in the possession of the carrier. The inventory in transit that is owned by UNDP (based on INCOTERMS 2020) must be recorded as inventories. Therefore, it is very important to determine the ownership of inventory items in transit based on respective INCOTERMS 2020.

For example, for FCA Incoterms (short for “Free Carrier”), the title of goods passes to UNDP when the supplier delivers the goods to the carrier nominated by UNDP. In this case UNDP should recognize the inventory while in transit.

Refer to: UNDP Programme and Operations Policies and Procedures (POPP) on Inventory Management

Practice PointerGlobal Fund inventory

For the purpose of the Global Fund grants, examples of inventory are health products such as pharmaceuticals, medical consumables, and medical equipment. UNDP Country Offices (COs) are required to count and report Global Fund inventory items only in cases where complete control over the Global Fund inventory is exercised until final distribution to the beneficiaries. In these cases, UNDP manages the complete logistics of inventory management either directly or through contracted third parties. The UNDP Global Fund Partnership and Health Systems Team (GFPHST) reviews country arrangements and will confirm where inventory recognition is required.

There are different practices in exercising control over Global Fund inventories until they are finally distributed to the beneficiaries. The Country Offices might be required to count and report Global Fund inventory items, i.e., where UNDP is deemed to have full control over inventory in accordance with UNDP’s inventory policy and year end guidelines on financial year closure.

Important: if arrangements have changed in other countries (resulting in UNDP’s control over inventory), it will be the responsibility of the CO to inform the GFPHST, count the inventory and submit the required reports. If there are any questions, COs should contact their respective OFRM/Finance Business Advisor (FBA) Manager with the GFPHST in copy.

It is expected that all undistributed health products in the following scenarios should be reported as inventory at the end of a quarter if one or more of the control criteria are met:

- Inventory items held at UNDP Central or Regional Warehouses/ storage locations.

- Inventory items are held at Government Central or Regional warehouses/ storage locations.

- Inventory items are held at an SR’s warehouses who are contracted by UNDP for providing logistics.

- UNDP can control or dictate further distribution of the items held at the above locations.

- Items in stock are insured by either UNDP or Global Fund project funds.

- UNDP bears the risks of loss, theft, damage, spoilage, etc.

The relationships UNDP has with Sub-recipients (SRs) and Agents vary but the following underlying concepts should be used as a guide:

- Sub-recipients: According to standardized SR Agreements, the SR is in charge of the distribution and safeguarding of the inventory (inventory in SR/government warehouses and under their control) whilst UNDP acts in a monitoring and evaluation role. In these instances, the inventories will be expensed when procured and not treated as a current asset at the end of a quarter if not distributed. However, there are instances where according to the nonstandard agreements, UNDP is always in control of Inventories until it reaches the end users where control is transferred. Consequently, these will be regarded as UNDP inventory at a period end and recorded and reported as inventories under generic project 00039902.

- Agents: Where UNDP employs a third party to act on its behalf as an Agent to store and distribute health products to the end users, if UNDP still controls and administers the distribution i.e. decides who, where and when; and is responsible for any loss, damage or spoilage in transit before it reaches the final end users, then it should be regarded as UNDP inventory. At the point the inventory is officially handed over to the end users, it is no longer UNDP inventory. Again, this is dependent on the agreement UNDP has with the Agent. UNDP must examine the substance of the transaction, rather than the form of the agreement with other parties and ensure that control is demonstrated before recognizing and reporting inventories as assets.

Global Fund-specific count procedures:

The standard file-naming convention for the inventory count reports differentiates submission type between Global Fund and Non-Global Fund projects.

For Global Fund projects, medical items are bought centrally by the Copenhagen office. As such, column 22 (Valuation) should be the same as column 18 (cost). If the medical items are not bought centrally, then valuation must be estimated and documented.

Budget Revision

UNDP Programme and Operations Policies and Procedures (POPP) are followed for budget revisions. It is imperative to note, however, that specific Global Fund requirements must also be adhered to.

The purpose of the revision is to make substantive or financial adjustments and improvements to the project budget. A project document may be revised at any time by agreement among the signatories to the document with no impact on project budget.

A formal change in the design of the project is called a substantive revision. Substantive revisions are made in response to changes in the development context or to correct flaws in the design that emerge during implementation. Substantive revisions may be made at any time during the life of the project.

Based on the year-end combined delivery report, the multi-year work plan shall be revised as needed to ensure a realistic plan for the provision of inputs and the achievement of results. In Quantum, the budget amounts that were budgeted for but not spent in prior years should be re-allocated to current or future years. Within the year, in the interest of sound financial management, budgets must be kept up to date and aligned with agreed plans to accurately assess progress and performance. The total multi-year budget should not exceed the total approved detailed budget of the Global Fund.

Refer to the following guidance:

UNDP Programme and Operations Policies and Procedures (POPP) on Implementing a Project.

Global Fund

Global Fund policies and procedures are documented in:

Reprogramming and Sub-recipient Budget Reallocations

Reprogramming

Reprogramming is the process of changing the scope and/or scale of goals and objectives and/or key interventions of a Global Fund supported program. These programmatic changes should be reflected in changes to the Grant Confirmation, potentially including the performance indicators, targets, health products management template (HPMT), and the budget.

Reprogramming may be initiated by either the Country Coordinating Mechanism (CCM) and/or Principal Recipient (PR) or suggested by the Global Fund Secretariat and managed in consultation with CCM, PR(s) and technical partners. All reprogramming requests shall be endorsed by the CCM, and the Global Fund Country Team may require a Local Fund Agent (LFA) review of the request.

Reprogramming of a grant may be proposed at any time during the grant implementation.

A reprogramming request is classified as either “material” or “non-material” (Please refer to Global Fund Budgeting Guidelines Section on Budget Revisions – Grant Implementation). A reprogramming is considered material and should be referred to the Technical Review Panel (TRP) for review when:

- It contradicts the TRP’s original review and recommendation on the proposal (e.g., an intervention originally removed by the TRP is being reintroduced to the programme; there is a significant redesign or shift of balance of original proposal/programme i.e., a prevention programme is shifting to treatment; a key intervention is removed from the grant without evidence of alternative funding in the country); or

- An independent technical review of a reprogramming request is required to approve the case when there is a lack of agreement, significant gaps in evidence to support a reprogramming need, unexplained lack of impact, or difficult trade-offs in decision making; or

- In cases where additional Global Fund financing representing more than a 30 percent increase to the approved funding for the implementation period.

Non-material reprogramming requests fall outside the definition of materiality described above and are reviewed and approved by the Secretariat.

Project Management and Update in Quantum

UNDP Programme and Operations Policies and Procedures are followed for project management and project update in Atlas/Quantum. Please refer to POPP on Project management/Implement for further guidance.

Sub-recipient Management

This section of the Manual focuses on financial and operational management of Sub-recipients (SRs), particularly regarding cash transfer modalities. Programmatic, legal and substantive guidance relating to SR management is detailed throughout the Manual but particularly in the following sections: SR management, Legal framework, Procurement and supply management (PSM), Monitoring and evaluation (M&E), and Audit and investigations.

UNDP as Principal Recipient (PR) for Global Fund grants assumes the role of Implementing Partner (IP) through Direct Implementation (DIM). DIM is the modality whereby UNDP as IP takes on full responsibility and accountability for the effective use of UNDP resources and the delivery of outputs, as set forth in the project document. UNDP may identify a Responsible Party (RP) to carry out activities within a DIM project (SR for Global Fund Grants).

A RP is defined as an entity selected to act on behalf of UNDP based on a written agreement or contract to purchase goods or provide services using the project budget. In addition, the RP may manage the use of these goods and services to carry out project activities and produce outputs. All RPs are directly accountable to UNDP in accordance with the terms of their agreement or contract with UNDP.

The RP may follow its own procedures only to the extent that they do not contravene the principles of the UNDP Financial Regulations and Rules of UNDP. Where the financial governance of the RP does not provide the required guidance to ensure best value for money, fairness, integrity, transparency, and effective international competition, that of UNDP shall apply. Please refer to Refer to the UNDP Programme and Operations Policies and Procedures (POPP) on Direct Implementation.

The SR is contracted by the PR of the grant to assist in implementing programme activities. The PR is responsible for the oversight of implementation by the SR. SRs often play a pivotal role in the implementation of programme activities, the management of grant resources and the timely achievement of grant results. The SR’s specific role in performance-based funding is that, for periodic disbursements, the SR provides the PR with progress updates on the implementation of those activities for which it is responsible. SRs serve as RPs (Implementing Agent code in Quantum) for the UNDP project/budget.

It is important to distinguish between SRs and other entities that provide services for a project. The Global Fund provides the following guidance on this issue:

Harmonized Approach to Cash Transfer (HACT)

The Harmonized Approach to Cash Transfer (HACT) dictates policies and procedures for capacity assessment, cash transfer modality, audit, assurance and monitoring. HACT applies to government and civil society organization/non-governmental organization (CSO/NGO) participation in UNDP projects. At this time, UNDP-managed Global Fund projects are exempt from HACT, and capacity assessments are performed instead.

Before an entity can be engaged as Responsible Party (RP) on a UNDP project, a capacity assessment of that entity is performed. The following are key considerations for capacity assessment:

- Technical capacity- ability to monitor the technical aspects of the project;

- Managerial capacity– ability to plan, monitor and coordinate activities;

- Administrative capacity– ability to:

- Procure goods, services and works on a transparent and competitive basis

- Recruit and manage the best qualified personnel on a transparent and competitive basis

- Prepare and sign contracts

- Manage and maintain equipment; and

- Financial capacity– ability to:

- Produce project budgets

- Ensure physical security of advances, cash and records,

- Disburse funds in a timely, proper and effective manner

- Ensure financial recording and reporting

- Prepare, authorize and adjust commitments and expenses

The partner’s technical, managerial, administrative and financial capacities should be reassessed throughout the life of the project (preferably on an annual basis).

The HACT macro- and micro-assessments are the basis for selection of the cash transfer modality used for each IP or RP and the level of assurance activities used. The level of risk can differ from institution to institution, and the UNDP office should effectively and efficiently manage this risk for each national institution by:

- Assessing the institution’s financial management capacity throughout the life of the project;

- Applying appropriate procedures for the provision of cash transfers to the institution; and

- Maintaining adequate awareness of the institution’s internal controls for cash transfers through assurance activities.

For each institution the level of risk may change over time, and this may require appropriate changes in options for cash transfer modality, and audit and monitoring procedures. Sub-recipient (SR) capacity assessment is addressed in detail in the SR management section of the Manual.

HACT offers three cash transfer modalities:

- Direct cash transfer - UNDP advances cash funds on a quarterly basis (based on agreed work plan) to the RP, who in turn reports back expense through Funding Authorization and Certification of Expenditures (FACE) forms. Note that the recording of expenses, from requisition through to disbursement, occurs in the books of the RP. UNDP is pre-funding the activities with advances of cash. Please refer to UNDP Programme and Operations Policies and Procedures (POPP) on Direct Cash Transfers and Reimbursements).

- Direct payment - The RP carries out the procurement activity but requests UNDP to make the disbursement directly to vendors through FACE. In this arrangement, UNDP is undertaking only the fiduciary function (accounting and banking services, and the disbursement function) on behalf of the RP. Please Refer to POPP on Direct Payments.

- Reimbursement - Unlike direct cash transfer, a reimbursement arrangement is where UNDP pays the RP after it has made a disbursement based on the annual work plan. The RP needs prior consultation with UNDP before embarking on the pre-financing arrangement. Please refer to POPP on Direct Cash Transfers and Reimbursements.

Depending on SRs’ capacity, it is possible to use all modalities in the same project, for different activities and/or inputs. However, this is not recommended due to this approach’s inherent complexity.

Please refer to POPP on Harmonized Approach to Cash Transfers (HACT)

Direct Cash Transfers

The FACE form supports several important functions:

- Request for funding authorization: The section “Requests/Authorizations” will be used by the Implementing Partner (IP)/Responsible Party (RP) to enter the amount of funds to be disbursed for use in the new reporting period. UNDP can accept, reject or modify the amount approved.

- Reporting of expenses: The section “Reporting” will be used by the IP/RP to report to UNDP on the expenses incurred in the reporting period. UNDP can accept, reject or request an amendment to the expenses reported.

- Certification of expenses: The section “Certification” will be used by the designated official from the IP/RP to certify the accuracy of the data and information provided.

Please refer to the UNDP Programme and Operations Policies and Procedures (POPP) on Direct Cash Transfers and Reimbursements.

Practice PointerProcedures for advances to government or civil society organization (CSO) Sub-recipients (SRs)

- The SR must have a good financial system of recording accounting transactions with appropriate filing of financial documentation on the project.

- The SR should open a separate bank account (with no access to credit, and not used for investments) for the Global Fund project at central and provincial levels. (An existing bank account under the name of the SR may be used only with approval of the UNDP Programme Officer)

- Signatory Authority forms along with new bank account details to be submitted to UNDP prior to SR agreement signing. Bank account to operate with double signatures.

- Strict control on the account, including monthly/quarterly bank reconciliation.

- After the completion of the project, the account is closed and remaining funds reimbursed to UNDP.

- As per signed SR agreements, SRs must provide quarterly financial (FACE) and programmatic reports within 15 days after the end of each quarter unless otherwise agreed with UNDP. SRs should also submit a copy of the bank statement showing the closing cash balance for the relevant quarter. A reconciliation to the balance of cash funds available as shown in the FACE should be attached. In addition, SRs should submit details on transactions accounted in the FACE form as well as supporting documentation to support expenditures.

- During FACE verification conducted by the CO, the CO should ensure that funds are used only for the activities and inputs stated in the annual work plan and should follow UNDP’s policies and procedures as referred to in the project document and SR agreement. UNDP allows for variations of not more than 10 percent of any budget line item, provided that the total budget is not exceeded.

- Advances to SRs shall only be made in local currency. Requests for non-local currency payments should be submitted to UNDP HQ Treasury for appropriate approval as per UNDP POPP.

- Advances to SRs should be issued on a quarterly basis for no more than three months of the approved budget (initial advance to cover project set-up cost). This modality requires close monitoring by the CO to verify the correct use of the advanced funds for achieving the work plan targets.

- An SR’s request for an advance for a project can be approved if at least 80 percent of the previous advance given and 100 percent of all earlier advances have been liquidated. SRs can request an advance as soon as 80 percent of a previous disbursement and 100 percent of all earlier disbursements are liquidated, even if that happens well before the end of the quarter. Reporting requirements remain the same, whether at quarter end or an earlier date. Please note the flexibility of 3% or $5,000 (whichever is lower) provided for 80% rule in the Guide for AP Invoice Processing (refer to page 13).

- Should an SR have outstanding advances over one year old, no new advances should be given to that SR for ANY projects it is implementing until the advance in question is liquidated.

- Based on the review/verification of the FACE report, UNDP will either:

- Accept: sign and approve the FACE;

- Request amendment to the FACE from the SR; or

- Reject the FACE, keeping a copy on file, returning it to SR, giving reasons for rejection.

Practice Pointer- After FACE verification and approval, expenses should be recorded through a standard invoice, debiting expense accounts 7xxxx with the split by budget lines/tasks. The standard invoice should be applied against a prepayment invoice for the credit against account 16005. Application of prepayment should be done with the same accounting date as expenditure invoice lines.

- After FACE verification and approval, advances should be issued to Govt/CSO SRs charging account 16005 and the corresponding chart field combination (Operating Unit – Fund – Department – Responsible Party – Donor). Advances should be processed through a prepayment invoice (non-purchase order (PO) that reserves the funds advanced to the project (the payee is the SR, never an SR employee). A tick should be put in the prepayment invoice to allow application against the prepayment invoice. In the prepayment invoice, there is no need to split a total amount of prepayment by budget lines/tasks, the full amount can be posted under one budget line/task related to SR

Practice PointerPlease refer to:

- UNDP POPP on Accounts Payable for guidance on AP vouchers and APJVs.

- UNDP POPP on Direct Cash Transfers and Reimbursements.

Detailed Steps in Verification and Monitoring of SR Financial Reports and Records

Sub-recipient (SR) funding is provided based on performance, which includes project management and financial performance. SRs must keep up-to-date and accurate records and documents supporting expenses made within the SR agreement, and the approved work plan and budget.

- Original documents must be kept and provided to UNDP upon request

- UNDP will conduct verification missions to verify submitted financial report supporting documents. Verification can also be conducted in the UNDP office based on reports and documents provided by SR.

- As per SR agreement requirements, UNDP will hire an external auditor for auditing SR activity in relation to signed SR agreements (For more information, please refer to the following section of the Manual: SR Management )

- The Local Fund Agent (LFA) review may involve site visits to the SR

Common errors in SR reporting include:

- FACE not signed (or signed by someone not included in signatory authority forms)

- Sufficient supporting documents (as per the Monthly Financial Data Verification Of SR/SSRs checklist) for each financial transaction not attached

- Inaccurate financial reconciliation

- Incomplete variance explanation on budget versus actual expenditure sheet

- Incorrect UNDP Chart of Accounts or budget lines used for financial transactions

- Arithmetic errors

- Accrual base accounting used instead of cash-based accounting

- Bases for apportioned overhead costs of HQ not explained (i.e., rent or utilities sharing)

Eligible expenses are:

- Validated based on documentary evidence

- In line with the approved budget

- Used solely for programme purposes

- Consistent with terms and agreement of the SR agreement

- Incurred during the implementation period as set in SR agreement, workplan and its budget

- Pre-approved in writing by UNDP

- Compliant with competitive procurement processes and relevant financial and procurement procedures of the implementer

Ineligible expenses include goods and services that are:

- Expenditures incurred outside of the scope or period of the grant

- expenditures incurred outside of Implementation period or Closure period. Expenditures in breach of the grant agreement

- expenditures not approved in the budget, expenditures exceeding budgets outside the implementer’s flexibilities provided by the Global Fund Unsupported expenditures.

- Unsupported expenditures.

- absence of supporting documents

- insufficient and/or inappropriate supporting documents

- missing or inappropriate signatures/authorizations

- Expenditures compromised by prohibited practices

- falsified or fabricated documents

- diversion of assets to non-Programme use

- non-competitive tenders/collusion/inappropriate facilitation of payments

- Expenditures compromised by prohibited behavior: such practices that could be corrupt, fraudulent, coerciveExpenditures relating to other types of non-compliance or mismanagement of Grant Funds:

- non-compliant taxes

- expiration or spoilage due to negligence or mismanagement

- cancellation costs

- procurement irregularities. Prices more than the prevailing market prices. Inadequate contracting practices.

- non-compliance with quality assurance.

- failure to replace lost, stolen or damaged assets

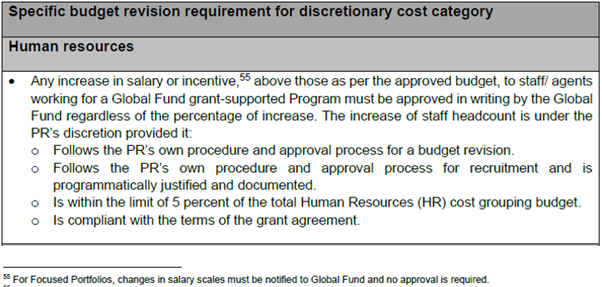

- non-complaint HR costs, increase in SR salaries or incentives without prior GF approval, etc.

Financial reporting (FACE) will include the following:

- FACE report

- Detailed information on transactions included in the FACE report

- Budget versus actual expenses analysis and explanations for variances

- Reconciliation of outstanding advances

- A bank statement reflecting expenses with closing balance as of reporting date and bank reconciliation

- A cash forecast for next quarter

- A copy of financial supporting documents against each transaction provided to UNDP along with the quarterly financial report

- A request for quarterly advance/disbursement

Minimum supporting documents for workshop/training include:

- Workshop agenda

- Signed & certified attendance sheet of participants

- Travel authorization form or travel itinerary

- Travel documents; boarding pass, air ticket, taxi bill

- Daily subsistence allowance (DSA) or per diem form

- If DSA and transportation costs of participants are paid in cash rather than through bank transfer as recommended, proper receipts from participants

Minimum supporting documents for M&E visits include:

- travel authorization form or travel itinerary

- travel documents: boarding pass; air tickets, taxi bills

- mission plan

- mission report

- DSA or per diem form

- If DSA and transportation costs of participants are paid in cash rather than through bank transfer as recommended, proper receipts from participants

Minimum supporting documents for salary payments include:

- attendance sheet, attendance report, individual staff time sheet

- Staff contracts

- Master payroll sheet

- Bank account copies

- Leave forms

- Payroll as per approved HR budget

Minimum supporting documents for local procurement include the ones listed below. For local procurement of health products, prior approval is required from the UNDP Global Fund Partnership and Health Systems Team (GFPHST).

- Approved purchase/service request form

- Assigned purchase committee form

- At least three quotations from market

- Bid-comparison statement

- Valid invoice

- Goods/service received note

- If payments to supplier are paid in cash rather than through bank transfer as recommended, proper receipts from supplier

The Monthly Financial Data Verification Of SR/SSRs checklist should be completed and signed. Outstanding or unresolved/disputed items should be escalated to the CO management as soon as possible or captured in risk register if the issues may lead to financial risks on grant performance.

Practice Pointer- Use of the direct payment modality to minimize currency risk associated with disbursing advances to SRs/Implementing Partners (IPs) in local currency.

- Monthly advances (rather than quarterly) to reduce the exposure between the time the advance is issued and the date the SR/IP spends the funds. As the local currency loses value at a high rate, funds disbursed at the beginning of the quarter would lose value before they could be used in the second and third month, negatively impacting the SR/IPs in meeting their targets.

- The SR advance balances should be kept minimal and the recording of the SR/IP FACE should be done using the monthly UN Operational Rate of Exchange (UNORE) (as opposed to the UNORE at the end of the quarter) to minimize unrealized exchange losses incurred on revaluation of SR advance balances.

Disbursement of SR advances in hard currency requires prior approval from the UNDP Treasurer.

COs should consult UNDP Crisis offer on the special measures that can be activated, depending on the country situation.

Reimbursements

This modality may be agreed to in cases where the Sub-recipient (SR) has sufficient resources to pre-finance activities.